LLC vs S-Corp vs C-Corp vs Sole Proprietor: How to Choose the Right Business Structure

Choosing the right business structure affects how much tax you pay, how much personal risk you take on, and how easily your business can grow. This guide explains how to choose the right business structure for your situation and when it makes sense to change as your business evolves. If you want the short version: most business owners don’t need the “perfect” structure on day one, they need the right structure for where they are now, with a clear plan to adjust later.

What is a business structure?

A business structure is the legal framework that determines how a business operates, is taxed, and is recognized under the law. It affects how much you pay in taxes, your personal liability, the forms you file, and your ability to raise capital.

What are the most common types of business structures?

The four most common business structures are sole proprietorship, partnership, limited liability company (LLC), and corporation.

How to Choose the Right Business Structure (Step-by-Step)

You can usually narrow down the right business structure by answering a few practical questions.

Step 1: How many owners will the business have?

- One owner → Sole Proprietor, LLC, or S-Corp election

- Multiple owners → Partnership, LLC, or Corporation

Step 2: Will the owners actively work in the business?

Active owners are taxed differently than passive investors, especially when payroll and self-employment taxes come into play.

Step 3: Do you need liability protection?

If there’s any meaningful risk: contracts, clients, employees, or debt, then liability protection matters.

Step 4: Will you seek outside investors?

Some investors require a specific structure (often a C-Corporation).

Step 5: How much profit do you expect in the next 12 months?

Expected profitability often determines whether advanced tax strategies make sense.

Step 6: Do you prefer simplicity or tax optimization?

Some structures are easier to maintain. Others require more compliance but may reduce taxes.

Step 7: Are you prepared for additional compliance?

Payroll, tax filings, and recordkeeping increase with certain structures.

In practice, many single-owner businesses start as an LLC and later consider an S-corporation tax election once profits increase.

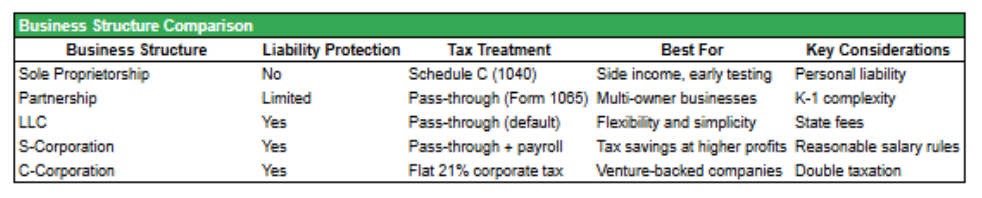

Business Structure Comparison

Sole Proprietorship

A sole proprietorship is the simplest business structure. There is no separate legal entity, you and the business are the same for legal and tax purposes.

Best for:

- Freelancers

- Side businesses

- Testing an idea with minimal risk

Pros:

- No formal setup required

- Simple tax reporting

Cons:

- No liability protection

- All profits subject to self-employment tax

- Harder to scale or bring on partners

Sole proprietorships are often a temporary starting point, not a long-term structure.

Partnership

A partnership is used when two or more people operate a business together without forming a corporation.

Best for:

- Multi-owner businesses

- Professional services firms

Pros:

- Flexible ownership

- Pass-through taxation

Cons:

- More complex tax filings

- K-1 reporting for owners

- Potential liability exposure without proper agreements

Most partnerships benefit from clear operating agreements and careful tax planning.

Limited Liability Company (LLC)

An LLC is one of the most common business structures for small and mid-sized businesses.

Best for:

- Business owners seeking flexibility

- Owners who want liability protection without heavy administration

Pros:

- Liability protection

- Flexible tax treatment

- Fewer formalities than corporations

Cons:

- State filing and annual fees

- Self-employment taxes still apply by default

LLCs are often used as a foundation structure, with tax treatment adjusted later as the business grows.

S-Corporation: Business Structure or Tax Election?

One of the most common points of confusion is the difference between an LLC and an S-Corporation.

An LLC is a legal business structure formed at the state level.

An S-Corporation is a federal tax election made with the IRS.

This means a business can operate as an LLC while being taxed as an S-Corporation.

Why business owners consider an S-Corporation election:

- Potential payroll tax savings

- Separation of salary and distributions

- Better alignment once profits grow

Trade-offs:

- Payroll is required

- Reasonable compensation rules apply

- More complex tax filings

An S-Corporation election is often considered when a business becomes consistently profitable and the owner is actively working in the business, but it is not right for every situation.

C-Corporation

A C-Corporation is a separate legal and tax entity from its owners.

Best for:

- Venture-backed startups

- Businesses planning to reinvest profits

- Companies seeking outside equity investment

Pros:

- Flat 21% corporate tax rate

- Easier to raise capital

- Clear separation between owners and business

Cons:

- Double taxation on profits and dividends

- More administrative requirements

- Not always tax-efficient for small owner-operated businesses

C-Corporations are powerful in the right context, but unnecessary for many small businesses.

Frequently Asked Questions

Should I start as an LLC and switch later?

Yes. Many businesses start as an LLC for simplicity and later elect S-Corporation tax treatment as profits grow.

What’s the difference between an LLC and an S-Corp?

An LLC is a legal entity. An S-Corporation is a tax election. An LLC can choose to be taxed as an S-Corp if it meets IRS requirements.

Do I need an EIN as a sole proprietor?

Not always, but an EIN is required if you have employees, certain retirement plans, or want to avoid using your Social Security number.

When does a C-Corporation make sense?

C-Corporations are typically used by businesses seeking venture capital or planning to reinvest profits rather than distribute them.

Choosing the Right Structure Is Only Step One

Your business structure should support your:

- Tax strategy

- Cash flow

- Risk tolerance

- Long-term goals

The right structure today may not be the right structure two years from now, and that’s normal.

The key is choosing intentionally and reviewing your structure as your business grows.