How to Calculate Quarterly Estimated Taxes for Business Owners

A practical guide to calculating and paying quarterly estimated taxes for business owners with W-2 income, business entities, and real estate.

If you are a business owner, estimated taxes are rarely straightforward.

You might have:

- One or more businesses (LLC, S-corp, C-corp, or Partnership)

- A W-2 salary

- 1099 income

- Rental real estate

- Investment or capital gain income

And the biggest mistake business owners make with estimated taxes isn’t math, it’s treating each income source separately instead of planning for them together.

This guide explains:

- When business owners must pay estimated taxes

- How estimated taxes interact with W-2 withholding

- Entity-specific considerations (S-corp, partnership, C-corp, LLC)

- How real estate income affects quarterly payments

- How to avoid penalties without overpaying the IRS

Why estimated taxes are confusing for business owners

Estimated taxes exist because the IRS expects tax to be paid as income is earned, not once a year.

Employees pay automatically through withholding.

And business owners often don’t.

What complicates things for business owners is that:

- Some income has withholding (W-2 wages)

- Some income doesn’t (distributions, K-1s, rent, 1099s)

- Cash flow ≠ taxable income

- Depreciation and entity structure change the timing of tax

Estimated taxes are the tool that solves this problem, when used correctly.

Do business owners actually need to pay estimated taxes?

You generally need estimated payments if both are true:

- You expect to owe $1,000 or more in federal tax after withholding, and

- Your withholding alone won’t cover the required amount for the year

Most business owners meet these conditions at some point.

Common situations that trigger estimated taxes

- S-corp owners with reasonable salary + distributions

- Partnership or LLC members receiving K-1 income

- W-2 income earners with a profitable side business

- Real estate owners with taxable rental income

- Owners selling assets or businesses during the year

The safe-harbor rules (your penalty shield)

The IRS won’t penalize you for underpayment if you meet one of these thresholds through withholding and estimated payments:

- 90% of your current-year total tax, or

- 100% of prior-year total tax (110% if prior-year AGI exceeded $150,000)

This matters because safe harbor allows planning flexibility.

Business owner insight: Early in the year, we usually use the prior-year safe harbor amount to set estimated payments. Once the business has a few months of data and profit trends are clearer, we adjust estimates to align with the actual projected outcome.

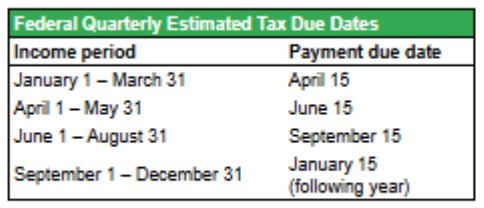

Quarterly due dates (and why they matter more than you think)

The IRS doesn’t divide the year into equal quarters.

Each payment covers income earned during a specific period, and penalties are assessed per period, not annually.

If a due date falls on a weekend or federal holiday, the payment is due on the next business day.

Important: Paying late in the year does not automatically fix underpayments from earlier quarters.

How estimated taxes work with W-2 withholding (critical for business owners)

Key rule

Withholding and estimated taxes are combined when determining whether you paid enough.

Tax planning advantage

W-2 withholding is generally treated as paid evenly throughout the year, even if it happens later.

That means:

- Increasing withholding late in the year can reduce underpayment penalties

- Owners with payroll control (especially S-corp owners) have more flexibility

Example

An S-corp owner:

- Pays themselves a reasonable salary

- Increases withholding in Q4

- Uses withholding strategically instead of large Q1–Q3 estimates

This is often more efficient than making large estimated payments.

Entity-specific estimated tax considerations

S-Corporations

- The entity does not pay federal income tax

- Owners pay tax on:

- W-2 wages (with withholding)

- Pass-through income (via estimates or withholding)

- Distributions themselves aren’t taxed, but the income behind them is

Partnerships & multi-member LLCs

- Income flows through via K-1

- No withholding unless specially elected

- Estimated taxes are usually required at the owner level

Tax planning note: Uneven profit distributions often justify the annualized income method.

Single-member LLCs / sole proprietors

- Income reported on Schedule C

- Subject to income tax + self-employment tax

- Estimated payments almost always required once profitable

C-Corporations

- The corporation pays its own estimated taxes

- Owners may still owe personal estimated taxes on:

- Dividends

- W-2 wages

- Other income sources

C-corp estimates are calculated and paid separately from personal estimates.

Real estate income and estimated taxes

Rental real estate complicates estimates because:

- Depreciation can eliminate taxable income

- Cash flow can exist without tax

- Bonus depreciation and cost segregation shift timing

What matters for estimates

- Taxable rental income, not cash flow

- Timing of asset purchases and depreciation elections

- Passive activity rules and grouping elections

Many real estate investors overpay estimates because they ignore depreciation until filing.

Uneven income? Use the annualized income method

Business income is rarely earned evenly.

If your income is:

- Seasonal

- Commission-based

- Deal-driven

- Back-loaded later in the year

You may reduce or eliminate penalties using Form 2210 (Schedule AI).

This method matches required payments to when income was actually earned, not when it eventually showed up.

How business owners should calculate estimated taxes

Each quarter, we recommend business owners:

- Estimate full-year taxable income across all sources

- Project total federal tax

- Determine safe-harbor target

- Subtract:

- Withholding already paid

- Prior estimated payments

- Pay the difference by the deadline

This helps prevent both:

- Surprise balances due

- Recurring IRS overpayments

What if you missed or underpaid an estimate?

You still have options:

- Pay immediately to reduce interest

- Increase W-2 withholding

- Apply the annualized income method

- Adjust future quarters strategically

Ignoring it is almost always the worst option.

Estimated taxes are a planning tool

When done correctly, making your estimated taxes payments can:

- Reduce or eliminate underpayment penalties

- Improve cash flow throughout the year

- Prevent unpleasant surprises at filing time